Corporate Estate Bond

How the Corporate Estate Bond Works

Your situation

Your company is an operating company or an investment holding company. It has retained profits or surplus cash that is not paid to you, since you do not need the income. Your corporation invests the cash in GIC's or other taxable investments, which you earmark for your heirs or favourite charity. You want a financial planning strategy that will increase the funds available when you die.

An option to consider -- the Corporate Estate Bond

This financial planning strategy requires your corporation to use its surplus cash to purchase a life insurance policy. By replacing the taxable investments with a life insurance policy, you will increase the funds available to your heirs when you die, reduce the amount of current and future tax your corporation pays, anc create a mechanism to move funds out of your corporation free when you die.

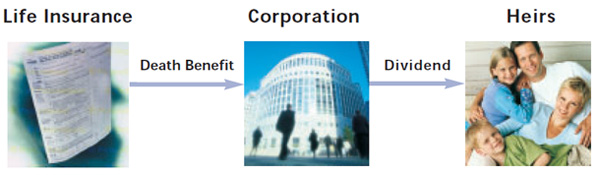

How does the Corporate Estate Bond work?

Your corporation purchase a life insurance policy on your life and is the beneficiary of the policy. The corporation deposits funds into the policy in excess of what is needed to pay the policy charges, creating cash value. This cash value accumulates on a tax deferred basis, increasing the death benefit payable under the policy. When you die, your corporation receives the proceeds of the policy, tax free. The corporatio receives a credit to its capital dividend account for the amount of the life insurance proceeds, less the insurance policy's adjusted cost basis. Dividends can then be paid -- tax free -- to your estate out of the capital dividend account.

By taking advantage of the Corporate Estate Bond, you have moved corporate investement dollars from a tax-exposed environment to a tax-sheltered environment, increasing the amount you give to your heirs of favourite charity when you die.

| Policy Value Projection | |||||||||

| Coverage Year | Insured Age | Assumed Primary Rate of Return(%) | Total Rate of Return (Including Bonus) (%) | Total Annual Planned Premiums | Fund Value | Cash Value | Annual Charges | Total Death Benefit | Side Account Balance |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 51 | 5.000 | 6.250 | 68,764 | 67,892 | 34,892 | 2,650 | 1,067,892 | 0 |

| 2 | 52 | 5.000 | 6.250 | 56,960 | 127,204 | 77,204 | 2,900 | 1,127,204 | 0 |

| 3 | 53 | 5.000 | 6.250 | 56,325 | 189,406 | 123,406 | 3,160 | 1,189,406 | 0 |

| 4 | 54 | 5.000 | 6.250 | 58,446 | 257,388 | 174,388 | 3,460 | 1,257,388 | 0 |

| 5 | 55 | 5.000 | 6.250 | 29,661 | 299,727 | 232,727 | 3,790 | 1,305,693 | 0 |

| 6 | 56 | 5.000 | 6.250 | 17,346 | 331,669 | 291,669 | 4,385 | 1,363,640 | 0 |

| 7 | 57 | 5.000 | 6.250 | 31,667 | 379,834 | 355,834 | 4,950 | 1,425,959 | 0 |

| 8 | 58 | 5.000 | 6.250 | 27,681 | 426,291 | 426,291 | 5,476 | 1,494,762 | 0 |

| 9 | 59 | 5.000 | 6.250 | 54,144 | 502,227 | 502,227 | 6,103 | 1,565,351 | 0 |

| 10 | 60 | 5.000 | 6.250 | 56,414 | 584,543 | 584,543 | 6,626 | 1,639,718 | 0 |

| 15 | 65 | 5.000 | 6.250 | 0 | 749,365 | 749,365 | 7,671 | 1,401,389 | 0 |

| 20 | 70 | 5.000 | 6.250 | 0 | 969,766 | 969,766 | 7,887 | 1,360,159 | 0 |

| 25 | 75 | 5.000 | 6.250 | 0 | 1,261,801 | 1,261,801 | 11,512 | 1,609,461 | 0 |

| 30 | 80 | 5.000 | 6.250 | 0 | 1,619,631 | 1,619,631 | 18,949 | 1,867,957 | 0 |

| 35 | 85 | 5.000 | 6.250 | 0 | 2,099,826 | 2,099,826 | 8,997 | 2,124,826 | 0 |

| 40 | 90 | 5.000 | 6.250 | 0 | 2,825,040 | 2,825,040 | 4,271 | 2,850,040 | 0 |

| 45 | 95 | 5.000 | 6.250 | 0 | 3,801,043 | 3,801,043 | 5,675 | 3,826,043 | 0 |

| 50 | 100 | 5.000 | 6.250 | 0 | 5,114,683 | 5,114,683 | 7,554 | 5,139,683 | 0 |

| This projection is based on an assumed weighted average primary rate of return indicated above and the marginal tax rate indicated in Section 1- Insurance Coverage Summary. | |||||||||

| The accumulation in this illustration is reported on a tax-deferred basis. However, please note that the growth of the money held in the Side Account is subject to annual tax reporting. | |||||||||

| The Bonus Amount is credited to the Fund Value on the first day after the applicable policy anniversary. | |||||||||

| The "Rate of Return" assumptions used in this illustration to estimate projected values for Index Interest Options are net of the contractual Interest Option Fee and, where applicable, the management fees & expenses (MER) and related GST of the underlying mutual fund. The Interest Option Fee is fixed and guaranteed not to change for each Managed Index Interest Options and Passive Index Interest Options. Transamerica reserves the right to change the Interest Option Fee applicable to any Passive Currency Neutral Index Interest Option subject to a Guaranteed Total Fee. Additional Information related to the Interest Option Fees can be found in the policy contract and in the Index Interest Option Fact Pages within the Transamerica website transamerica.ca | |||||||||

| Additional information about index interest options including historical rates of return can be found on the Transamerica website transamerica.ca where you can also find the detailed Index Interest Option Fact Pages. | |||||||||